“Nothing is secure but life, transition, the energizing spirit.” -- Ralph Waldo Emerson

As investors continue to position portfolios following the Fed's QE3 announcement of unlimited mortgage backed securities buying, it appears there is quite a bit of movement occurring on the long-end of the Treasury curve. Expectations for QE3 were for a more aggressive Treasury bond buying program, which helped push Treasury prices ever higher and yields lower. Those expectations partially got dashed following the actual announcement, sending the 30-Year Treasury yield soaring to over 3% in the blink of an eye. However, in recent days, a meaningful recovery in Treasury prices has occurred as investors question whether monetary action will force reflation or not.

Stock And Bond Hybrids

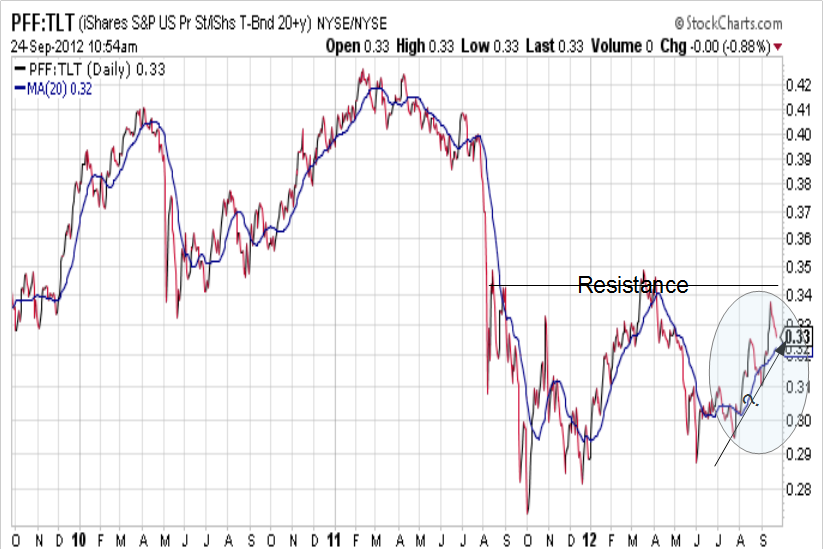

I do not believe this is a harbinger of bad things to come just yet. Money seems to be more and more comfortable with risk-taking, and high yielding areas of the bond market continue to perform well. As the Fed crowds money out of certain areas of the investable landscape, it is going elsewhere. One of the areas that is benefiting clearly appears to be in the “hybrid” of stock and bond investments known as Preferreds. Take a look below at the price ratio of the iShares S&P US Preferred Shares ETF (PFF) relative to the iShares 20+ Treasury Bond Fund (TLT). As a reminder, a rising price ratio means the numerator/PFF is outperforming (up more/down less) the denominator/TLT.

Strength Ahead

Notice that the trend has been fairly strong favoring Preferreds as an income and capital appreciation play relative to Treasuries since the end of May and before the June 4 low in risk assets, and that the ratio is now hitting up against resistance. I suspect this is a retest to the trend line, and that continued strength seems likely in the coming months. I say this because of continued leadership in Financials (XLF), which make up a substantial portion of the PFF ETF. Our ATAC strategies used for managing client accounts also remains favorably inclined towards equities. Given that central banks have committed themselves to forcing reflation, it seems ever more likely that the time for Treasuries is likely over, and that money will continue to take more risk in non-bond investments. Preferreds seem to be the transitional vehicle of choice for now to do that.

This writing is for informational purposes only and does not constitute an offer to sell, a solicitation to buy, or a recommendation regarding any securities transaction, or as an offer to provide advisory or other services by Pension Partners, LLC in any jurisdiction in which such offer, solicitation, purchase or sale would be unlawful under the securities laws of such jurisdiction. The information contained in this writing should not be construed as financial or investment advice on any subject matter. Pension Partners, LLC expressly disclaims all liability in respect to actions taken based on any or all of the information on this writing.

As investors continue to position portfolios following the Fed's QE3 announcement of unlimited mortgage backed securities buying, it appears there is quite a bit of movement occurring on the long-end of the Treasury curve. Expectations for QE3 were for a more aggressive Treasury bond buying program, which helped push Treasury prices ever higher and yields lower. Those expectations partially got dashed following the actual announcement, sending the 30-Year Treasury yield soaring to over 3% in the blink of an eye. However, in recent days, a meaningful recovery in Treasury prices has occurred as investors question whether monetary action will force reflation or not.

Stock And Bond Hybrids

I do not believe this is a harbinger of bad things to come just yet. Money seems to be more and more comfortable with risk-taking, and high yielding areas of the bond market continue to perform well. As the Fed crowds money out of certain areas of the investable landscape, it is going elsewhere. One of the areas that is benefiting clearly appears to be in the “hybrid” of stock and bond investments known as Preferreds. Take a look below at the price ratio of the iShares S&P US Preferred Shares ETF (PFF) relative to the iShares 20+ Treasury Bond Fund (TLT). As a reminder, a rising price ratio means the numerator/PFF is outperforming (up more/down less) the denominator/TLT.

Strength Ahead

Notice that the trend has been fairly strong favoring Preferreds as an income and capital appreciation play relative to Treasuries since the end of May and before the June 4 low in risk assets, and that the ratio is now hitting up against resistance. I suspect this is a retest to the trend line, and that continued strength seems likely in the coming months. I say this because of continued leadership in Financials (XLF), which make up a substantial portion of the PFF ETF. Our ATAC strategies used for managing client accounts also remains favorably inclined towards equities. Given that central banks have committed themselves to forcing reflation, it seems ever more likely that the time for Treasuries is likely over, and that money will continue to take more risk in non-bond investments. Preferreds seem to be the transitional vehicle of choice for now to do that.

This writing is for informational purposes only and does not constitute an offer to sell, a solicitation to buy, or a recommendation regarding any securities transaction, or as an offer to provide advisory or other services by Pension Partners, LLC in any jurisdiction in which such offer, solicitation, purchase or sale would be unlawful under the securities laws of such jurisdiction. The information contained in this writing should not be construed as financial or investment advice on any subject matter. Pension Partners, LLC expressly disclaims all liability in respect to actions taken based on any or all of the information on this writing.