It’s been a horrific week for weather for the eastern seaboard of the U.S., but the economic numbers remain encouraging. There’s still no sign that the economy is poised to break free of the slow-growth gravity field, but the numbers generally continue to support the view that a new recession isn't an imminent threat.

Consider Friday’s payrolls update for October -- private-sector jobs increased 184,000 last month on a seasonally adjusted basis. That’s the best monthly gain since February and a sign that the labor market is still growing, and perhaps at a slightly faster rate. It’s not growing fast enough to inspire rosy forecasts, but the expansion continues to roll along.

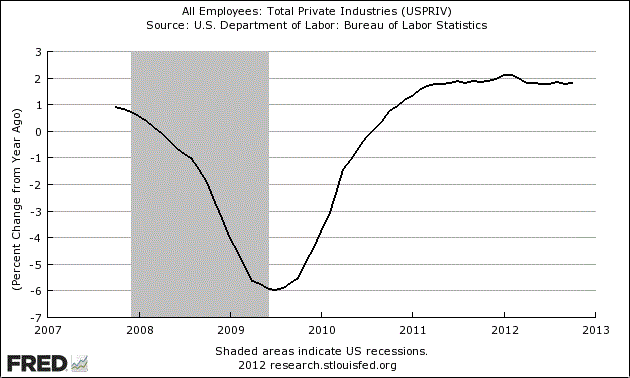

That’s also the message when we review the longer-term trend: the annual change in private payrolls rose 1.8% through last month, or roughly at the pace that we’ve seen since April (see chart below). That’s a sign that nothing much has changed in the nation’s capacity for minting new jobs: the middling expansion is still with us, despite what you may have heard elsewhere.

Thursday’s weekly release for initial jobless claims also provides modestly good news on the margins: a 9,000 decline in new filings for jobless benefits to a seasonally adjusted 363,000. That still leaves new claims more or less unchanged from the past several months, but the fact that claims aren’t rising is a good sign for broad outlook.

Even better, the annual percentage change in new jobless claims before seasonal adjustment suggests that the slow healing for the labor market persists. Unadjusted claims fell 8.1% last week vs. a year ago. The rate of a decline is a bit slower than we’ve seen in recent months, but it’s still decent progress and one more data point on the side of optimism.

So is the news that manufacturing improved slightly last month, according to the Institute for Supply Management. “Economic activity in the manufacturing sector expanded in October for the second consecutive month following three months of slight contraction,” ISM reports in a press release. The ISM Manfacturing Index rose to 51.7 in October, up from 51.5 previously. That's far from a boom, but any reading above 50 implies economic growth. This is the second month of 50-plus territory and it lends further support for arguing that the summer slump for this index hasn't spilled over into the fall.

All of this should be considered in context with a broader review of the economy. A few weeks back, The Capital Spectator Economic Trend Index (CS-ETI) told us that recession risk was low, based on numbers through September. This week’s data releases imply that more of the same may be on tap for October. Yes, it’s still early and there’s a long road ahead for October's economic updates, but so far, so good.

To be sure, economic growth remains modest at best and there are still plenty of risks lurking around the world. But based on the data that’s published to date, the path of least resistance continues to look encouraging. That could change, of course, and perhaps quickly, but for now let’s recognize what’s been obvious for months: recession risk doesn’t look threatening because slow growth prevails.

- English (UK)

- English (India)

- English (Canada)

- English (Australia)

- English (South Africa)

- English (Philippines)

- English (Nigeria)

- Deutsch

- Español (España)

- Español (México)

- Français

- Italiano

- Nederlands

- Português (Portugal)

- Polski

- Português (Brasil)

- Русский

- Türkçe

- العربية

- Ελληνικά

- Svenska

- Suomi

- עברית

- 日本語

- 한국어

- 简体中文

- 繁體中文

- Bahasa Indonesia

- Bahasa Melayu

- ไทย

- Tiếng Việt

- हिंदी

A Decent Week For Economic News

Published 11/02/2012, 02:46 PM

Updated 07/09/2023, 06:31 AM

A Decent Week For Economic News

3rd party Ad. Not an offer or recommendation by Investing.com. See disclosure here or

remove ads

.

Latest comments

Install Our App

Risk Disclosure: Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

© 2007-2024 - Fusion Media Limited. All Rights Reserved.